‘The time has come for policy to adjust’: Powell says rate cuts imminent

For the first time in definitive terms, Federal Reserve Chair Jerome Powell said it is time to cut rates after witnessing “unmistakable” cooling in the labor market. Powell made the remarks Friday, Aug. 23, at the Kansas City Fed’s annual economic symposium in Jackson Hole, Wyoming.

“The time has come for policy to adjust,” Powell said. “The direction of travel is clear and the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks.”

“We will do everything we can to support a strong labor market as we make further progress toward price stability with an appropriate dialing back of policy restraint,” Powell added. “There is good reason to think that the economy will get back to 2% inflation while maintaining a strong labor market.”

Despite the optimism, the labor market is undoubtedly slowing. In July, the unemployment rate spiked up to 4.3%, triggering a recession indicator. And the latest Labor Department revisions showed the Bureau of Labor Statistics overestimated job growth by 818,000 for jobs added throughout the year ending in March.

“The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions,” Powell said.

Given the remarks, markets are practically using permanent ink to mark a September rate cut. The Federal Open Market Committee, which sets the overnight lending rate, will meet three more times this year. Powell left the size and pace of rate cuts open to interpretation.

Is Powell’s ‘soft landing’ slipping away? Job worries cloud Jackson Hole speech

Jackson Hole, Wyoming, is known for its temperate summers, but Federal Reserve Chair Jerome Powell is probably feeling the heat turn up a bit ahead of his most-anticipated speech of the year. Powell will speak Friday, Aug. 23, at the Kansas City Fed’s annual economic symposium at Grand Teton National Park.

“This is his opportunity to send us a clear message on some aspect of what the Fed is thinking about,” Kathleen Hays, editor-in-chief of Central Bank Central, said. “I don’t think it’s going to be just looking at the economy and inflation. He’ll probably put this in a bigger context. At the same time, I think people are going to be waiting for him to just give us a little more guidance on where you’re leaning now.”

On Wednesday, the Fed released minutes from the latest Open Market Committee meeting in July. It decided to keep rates the same two days before a disappointing jobs report rocked people’s views of the labor market.

According to the minutes, the vast majority of people in that meeting expressed that it would likely be appropriate to cut rates in September. That said, several made comments that they could have also gotten behind a cut in July, which didn’t happen.

But here’s the kicker: Many participants noted that reported payroll gains might be overstated, and some noted the easing labor market faced a higher risk of more serious deterioration.

Now, it is confirmed that payroll gains have been overstated, just as many of those Fed members suspected.

“Since January of 2023, we’ve seen one downward revision after another to the data — it’s become systematic,” QI Research CEO Danielle DiMartino Booth told Straight Arrow News in August.

The latest Labor Department revision shows the U.S. economy added 818,000 fewer jobs than previously reported over 12 months ending March 2024. That’s about a 30% hit to what the Bureau of Labor Statistics initially released. It doesn’t mean those jobs were lost, it means they were never there in the first place. Therefore, while the labor market was still strong over those 12 months, it wasn’t on quite the tear the initial data indicated. These estimates will not be finalized until February 2025.

“And it takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data for GDP,” DiMartino Booth noted of revisions.

All of these moving parts are putting the Fed’s soft landing scenario at risk. A soft landing is being able to come down from too-high inflation without triggering a recession.

Inflation has come down quite a bit. The Fed’s preferred inflation measurement (core PCE) is at 2.6%, close to its 2% target. And the softening labor market is all the more reason to act.

In Powell’s speech Friday listeners will hope to hear from him that a soft landing is still in sight.

“We know the Fed’s going to be cutting rates,” Hays said. “We know they’re going to normalize. So it’s more of a question of when and how much and how fast.”

Complicating matters is the upcoming election. The Federal Reserve is a politically independent body and it would never want to be seen as carrying water for one party or another.

There is only one meeting before the election, on Sept. 17-18. Taking politics out of it, most economic signs point to the need to cut rates in September. But that will likely give the economy a boost, and that’s why in an interview with Bloomberg, Donald Trump said cutting before the election is “something that they know they shouldn’t be doing.”

The next Fed meeting starts the day after Election Day, but the Fed may not wait that long with the labor market showing these cracks.

Fed cutting rates before September like ‘yelling fire in a crowded theater’

Many argue the Federal Reserve missed the boat after failing to cut rates to ease financial conditions two days before latest jobs report triggered a recession indicator on Friday, Aug. 2. The Federal Open Market Committee is not scheduled to meet again until Sept. 17-18.

Now, experts are making the case for deeper rate cuts in light of rising unemployment. Some are even suggesting the Fed issue an emergency rate cut between now and the September meeting.

It would, at this point, be akin to yelling fire in a crowded theater if they were to come in with an emergency rate cut.

Danielle DiMartino Booth, CEO, QI Research

Former Fed adviser and CEO of QI Research Danielle DiMartino Booth said that while the Fed is behind the ball, an emergency cut would do “more harm than good.” In an interview with Straight Arrow News, she talked about the signs Fed Chair Jerome Powell missed that led to July’s decision.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Simone Del Rosario: I know you have been warning about these underlying symptoms of recession for some time. The Fed chose not to cut in July and then two days later had this jobs report that wrecked the markets for a moment. Where are you? Are they okay to wait until September to cut? Do you want to see something from them in the meantime?

Danielle DiMartino Booth: It would, at this point, be akin to yelling fire in a crowded theater if they were to come in with an emergency rate cut. Those are usually reserved for end of the world type of moments, financial pandemics, financial crises, credit events. So I think at this point it would do more harm than good.

I was strongly of the mind that they should have cut rates at the July meeting. At the podium, when he was pressed, [Fed] Chair [Jerome] Powell did acknowledge that there was a discussion about whether or not to cut rates in July. So you know that even though the decision was unanimous, there were no dissents, that there were some who believed that they should have started in July.

This is nothing new, companies aggressively laying off. Again, it’s been occurring for most of 2024 and yet [Powell has] been ignoring it.

Danielle DiMartino Booth, CEO, QI Research

There’s a company called MacroEdge and they do a very transparent job of tracking job cut announcements. We’ve had an average of 100,000, more than 100,000 job cuts announced over the last four or five months here in a time of the year that is typically benign. Usually you see your worst month of the year be January, that’s when the CEO and the CFO come in and clean house. But April was worse and it’s been just awful ever since then. For heaven’s sake, we’re seven days into the month of August and we’ve already seen 40,000 job cuts announced.

We’re talking about Jay Powell here, he founded the Industrial Group when he was at The Carlyle [Group]. He speaks to lot of CEOs. He knows that they’re in the process of reducing their head count. So just in terms of data on the ground, anecdata, it’s all around him and it’s been all around him.

This is nothing new, companies aggressively laying off. Again, it’s been occurring for most of 2024 and yet he’s been ignoring it. So I really do think that he should have [cut rates] on July 31.

The reason I think that we’ve seen the Wall Street Journal mention 50 basis points is because that’s now become a base case for September 18 or we wouldn’t have read it in the Wall Street Journal.

Simone Del Rosario: We are going to get another month of jobs data before the Fed meets again. What sort of labor picture do you think it’s going to paint when we look up the first Friday of September to see what happened in August?

Danielle DiMartino Booth: I mean, anything is possible with this Bureau of Labor Statistics. I’m done guessing what they’re going to do and what they’re going to report. When the data is eventually revised by law, we see where it really, really is.

For me at least, because there is this systematic downward revision of the data, I just feel like it’s a politicized institution at this point. And I don’t say that lightly, and I’m certainly not trying to be insulting to anybody inside the organization.

I just feel like [the Bureau of Labor Statistics is] a politicized institution at this point. And I don’t say that lightly.

Danielle DiMartino Booth, CEO, QI Research

But you typically see the unemployment rate continue to increase after it’s stopped rising by a tenth of a percentage point. It’s what you’ve seen in many, many recessions looking back: Initially there’s a very gradual rise in the unemployment rate and then it really starts to take off. And we are seeing companies being much more aggressive and large with their layoff announcements and it is actually manifesting in the jobless claims data as well.

Simone Del Rosario: Is it politicized or are they just not as accurate at this point? Is the survey outdated or do you firmly believe that there are underlying political reasons why the picture is rosier when they first paint it than it turns out to be later?

Danielle DiMartino Booth: Again, we are having this discussion in August 2024 and we’ve been seeing downward revisions since January 2023. If, at this point, there has not been an internal recognition that the model is broken and it’s been addressed, then it’s what we call willful blindness.

So at some point you have to recognize that something is broken and address it, not just ignore it, unless you’re ignoring it willfully. And again, I’m not trying to be insulting of the institution, but we’ve just seen a headline in a $25 trillion economy that funding for the household survey is going to be cut. That’s the most ridiculous thing I’ve ever heard in my life.

In a world in which we have big data, artificial intelligence, ways to streamline operations, make certain practices and methodologies more efficient, that we can’t better track the U.S. labor force, it just seems nonsensical to me.

Here’s why this former Fed adviser says we are already in a recession

The creator of a recession indicator that was triggered this past week said her rule is broken this time around and there’s no recession right now. But not everyone agrees. In fact, a different recession indicator points to the U.S. having entered a recession in October of last year.

“We’re not in a recession,” Sahm Rule creator Claudia Sahm told Straight Arrow News. “It’s never time to panic, but it’s also not recession time either. So it’s not a recession. And yet the risks are there.”

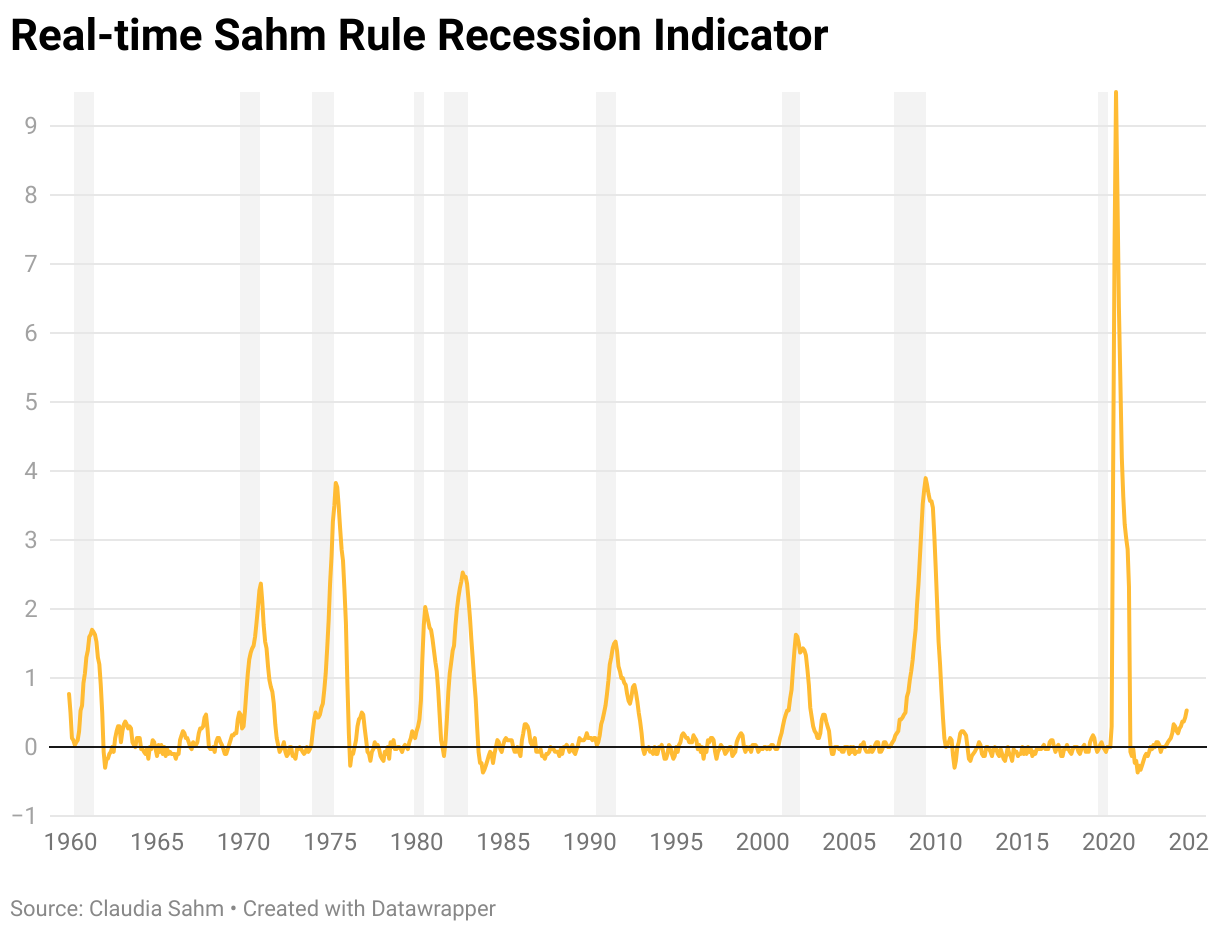

Recessions are declared by the National Bureau of Economic Research in hindsight by looking at the economy’s growth over previous quarters. Recession indicators like Sahm’s look at rising unemployment rate trends for more immediate indications the country has entered a recession.

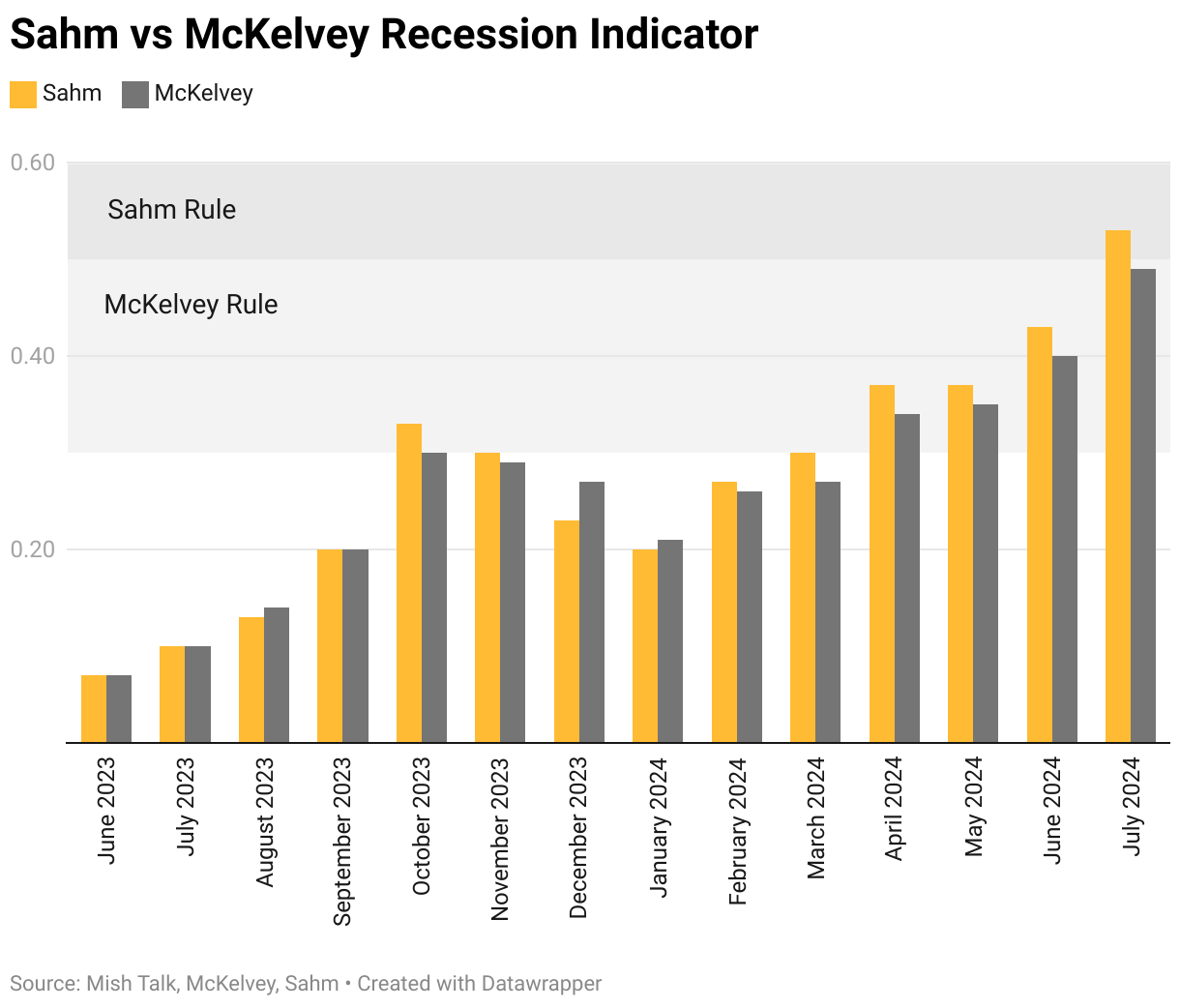

While Sahm’s rule was triggered by last week’s release of July’s jobs data, a different recession indicator was set off last October. In simple terms, the McKelvey Rule hits when the three-month average rise in unemployment hits 0.3 percentage points above the year’s low, compared to Sahm’s 0.5-percentage-point threshold.

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Danielle DiMartino Booth: I do think we’re in recession. Everything that we’ve seen from the Bureau of Labor Statistics with regards to the fourth quarter of 2023 indicates that they’re going to be revising into negative territory the final three months of 2023.

So that would stretch job losses from the third quarter of 2023 – when there were 192,000 jobs lost in the United States – that would stretch that into the fourth quarter and give us a six-month stretch of job losses upon revising the Bureau of Labor Statistics survey data with the hard data that we get from the Census Bureau, where companies are legally obligated once a quarter to report their headcount.

And that’s kind of the ultimate decision. That’s when the ink dries, if you will, on the payrolls data that we see the Bureau of Labor Statistics release.

Simone Del Rosario: So we’re looking at a recession that would have started in October of last year?

Danielle DiMartino Booth: I personally see the recession as having started in October 2023 because that’s the first time that the McKelvey Rule, which is less arduous than the Sahm Rule – and it doesn’t date back to 1948, it dates back to 1968 – but it has not missed a single recession since then.

Rather than a 0.5-percentage-point increase in the unemployment rate off of its lowest level in the prior 12 months, it is a 0.3-percentage-point increase in the unemployment rate over the prior 12-month period’s low.

Again, it has a spotless track record since 1968. It was triggered in October of 2023. The Bureau of Labor Statistics said that we lost 192,000 jobs in the three months ending Sept. 30, 2023. So the National Bureau of Economic Research could theoretically backdate it further, but again, the McKelvey Rule is what I’ve relied on.

The former chief economist at Goldman Sachs, he was interviewed by the Wall Street Journal in January 2008 when his rule was triggered, and he was asked the same question: ‘Well, your McKelvey Rule was triggered in December of 2007. Do you think we’re in recession?’ And he said, ‘Well, you know, my rule might be broken,’ basically.

But of course, the NBER did backdate that recession to December 2007 and the McKelvey Rule was not broken. Luckily, the Bloomberg Economics team agrees with me that recession, that job losses started in October 2023.

Simone Del Rosario: Why isn’t the Federal Reserve looking at these data points?

Danielle DiMartino Booth: I think the Fed is choosing to look the other way in this instance. There are some regulations that the Fed has been working on that could really define Chair Powell’s legacy – that would begin to regulate the private equities, the hedge funds, the BlackRocks of the world that are in some cases larger than banks if you consider the trillions of dollars that they have under management – and in order to push through with some of these regulations, he really does need higher-for-longer [rates] on his side.

He needs the higher-for-longer policy enough to go with what the Bureau of Labor Statistics first reports, even though we know that since January 2023, we’ve seen one downward revision after another to the data. It’s become systematic, in fact, the persistence with which we’ve seen downward revisions to what’s first reported. But again, I think [Fed Chair Jerome] Powell’s got his own reasons.

Simone Del Rosario: How do you square this idea that we could be in a recession right now with the GDP numbers that we’re seeing? The latest reading, the advance estimate, showed an annual growth rate of 2.8%.

Danielle DiMartino Booth: So we had 2-point-something percent in 2001 when it was first reported. Of course, it was another six quarters later that we revised it and found out that it was a negative number.

It takes magnitudes of the amount of time to get correct unemployment data, correct payrolls data. You can double the time that it takes to figure out what the actual GDP is that’s associated with that time frame.

If you find out that you’re 830,000 jobs shy of what you thought you were, which is what we found out in the third quarter of 2023 looking backward with hard data in hand, then you have to subsequently go back and back out. Well, 830,000 people were not actually working; 830,000 people were not actually producing the economic output that we thought we were. So you’ve got to back that out.

It takes a lot of time for the Bureau of Labor Statistics data to work its way into subsequent revisions for the Bureau of Economic Analysis data, for GDP.

It’s at inflection points. It’s when contractions become expansions, when expansions become contractions, that these big statistical agencies have trouble seeing the turning point, given their modeling.

But it wasn’t until 2018 that we saw the final GDP revision from the Great Recession that ended in June 2009. Again, the recession ended June 2009. We didn’t get the final revision for GDP for that recession until 2018.

Simone Del Rosario: On one hand, this can seem incredibly frustrating if people feel like we’re in a recession, they feel like the economy’s not good, and yet we continue to get, on the surface, economic releases that show a pretty strong economy. But that said, if, to your point, we are already in a recession, does that take some of the panic away since we’ve already been going through it, or is it going to get worse? What’s your read on that?

Danielle DiMartino Booth: Well, your average recession is 10 months long in the post-war era. So using that average length of time, we should theoretically be starting to recover and coming out of recession.

That being said, the Federal Reserve has waited now 12 months, now longer than 12 months, and the longer it waits, typically the deeper and longer the recession is as a result.

There have been some great studies that empirically demonstrate this. The period leading up to the Great Recession, 2007-2009, the Fed waited 15 months. It’s the longest the Fed’s ever waited.

So we’re just at the 12-month mark now. But it certainly looks like we’re going to get to the 14-month mark if it’s Sept. 18 that we can anticipate that first rate cut. So that’s about as long as the Fed has ever waited to provide relief in the form of the beginning of an easing cycle.

Why the Sahm Rule creator says the recession rule is wrong this time

Recession fears have dominated headlines since Friday’s jobs report, where the rising unemployment rate triggered a recession indicator known as the Sahm Rule. The rule has an incredible track record of signaling the start of a recession, yet this time is an outlier, according to the rule’s creator.

The Sahm Rule states a recession in the U.S. has started when the three-month average of the unemployment rate crosses 0.5% or more relative to its low from the previous 12 months. July’s surprise unemployment rate of 4.3% triggered the Sahm Rule with a 0.53% rise.

Asked point-blank whether the U.S. is in a recession, Claudia Sahm told Straight Arrow News, “No, we are not.”

It’s not a recession and yet the risks are there because we do have these increases in the unemployment rate.

Claudia Sahm, Chief Economist, New Century Advisors

The following transcript has been edited for length and clarity. Watch the full interview in the video above.

Claudia Sahm: We should be concerned that [the unemployment rate] has been rising over the past year. And this is not just about hitting a particular level, or in July, we saw a larger jump than we’ve seen. The Sahm Rule averages across months. It looks over a year-long period. So it’s trying to get this direction that we’re headed and it’s not a good direction.

Now there are some very specific reasons, very special reasons that the Sahm Rule right now looks more ominous than it is. And the first thing we can say about, “we’re not in a recession,” is anytime we make a pronouncement like that, we should look around.

And in fact, broadly speaking, this economy is still growing and a recession means that it’s contracting, right? So we still see consumer spending, we’re adding jobs, industrial production. It’s slowed down, it’s not growing as fast, but we’re still growing. So that’s not a recession – right now.

So what’s going on with the unemployment rate? So there’s the bad reason unemployment rate goes up is there’s less demand for workers, it gets harder to find jobs. Hiring rates have come down a lot. It is a lot harder if you’re on the outside trying to find a job right now. So the unemployment rate has gone up for a bad reason. It does that in recessions.

The unemployment right now is also going up for one of the good reasons. So we have had more people join the workforce who weren’t working before. In particular, there was a big increase in immigration. And that was so important for solving the labor shortages that we’ve been suffering through. And yet, it takes time to adjust. I mean, that should be the theme of this cycle since the pandemic, that big messy changes take time and it’s painful.

It can make it really hard to read where the economy is, but right now we have people who’ve come in, and for some of them, it’s just going to take time for them to find jobs. And in that period, the unemployment rate will go up. Once they find the jobs, it can come back down. And frankly, people coming in to work, that’s a good sign for keeping the economy growing because there are more workers. That extra piece of unemployment rate increase looks bad but actually, it’s probably not.

I can say, looking broadly, what we know about the economy, we’re not in a recession. I mean, it’s never time to panic, but it’s also not recession time either. So it’s not a recession and yet the risks are there because we do have these increases in the unemployment rate that are of the more problematic kind, we just don’t know exactly how much.

Simone Del Rosario: When you created this rule, it was so policymakers could act on signs of a recession. Looking at what’s happening right now, there’s obviously a major movement happening with unemployment. What’s the remedy?

Claudia Sahm: There is a very clear policy lever out there to be pulled and that is the Federal Reserve beginning to reduce interest rates. And that’s the most straightforward one at this point. And the Fed has told us they are pointed at doing that.

Before we found out about July’s employment report, that’s the path they were on. Seeing that there is probably more weakness or at least more slowing in the labor market than we had previously thought, that probably means that they can get going in September, and maybe even cut interest rates more quickly than they had expected.

And it’s important that they have that lever to pull. It’s so important that we’re still in a position of strength. We’re not in a recession, we are still growing, there’s a lot of good things in U.S. economy.

The direction is not good, right? We don’t need to soften or weaken more than we have and that’s kind of where we’re pointed. And the realization that the Fed has been putting pressure on the economy to slow it down and for them to say, “Okay, we don’t need to slow it down anymore,” and reduce risk, that is the release valve to this that can get us to a good place.

That we just kind of settle into the jobs catch-up, we keep growing, we stay away from the recession. That’s the path. And you can tell the story and the path is there. It’s just anytime you get close to these real risky places in the economy, like a recession, you have to be careful because the people can get scared, markets can react. Things can unfold in unpredictable ways. So I think people should have their guard up more than a typical time and yet, there’s still a path to this all being just fine.

Simone Del Rosario: Are you concerned about a near-term recession or are you confident that when the Fed pulls that lever, the risk is over?

Claudia Sahm: I’m a macroeconomist. I’m always concerned. I devoted much of my career to studying recessions and how to fight them. And so I think it’s a risk that we should always be aware of, or at least policymakers should certainly be aware of. It is not my base case.

And again, I don’t want to make light of the Sahm Rule. The pattern I identified, there are other similar people looking at labor market conditions, it’s not like I’m the only one who’s pointed to weakness right now.

It does have a really strong track record and I don’t want to dismiss it out of hand. Something is happening and I don’t want to just write off any of the bad signs because now would be the time to act on them. Given all that, I think the risks are there. They’re not overwhelming. And because we’re still in a position of relative strength, that gives us a real leg up in terms of like what happens over the next three months, six months, 12 months.

Simone Del Rosario: Did the Fed make a mistake last week by not cutting?

Claudia Sahm: I have made the argument for much of this year that the Federal Reserve should begin to gradually lower interest rates, that inflation was coming down. Yes, the beginning of the year was a little rough. We’re also learning that we probably got head-faked by some of that data. We might be getting head-faked by some of the employment data now. It might not be as bad as it looks, right? But there was definitely a case, inflation is coming down, the Federal Reserve should get out of the way.

I had said last week they should start gradually reducing rates because it would be so much better to gradually reduce interest rates, watch the effects on the economy, because there are many question marks. We don’t know exactly how this amount of interest rate cuts translates into that amount of spending. So just to kind of watch and see what the economy does.

Hindsight’s 20-20. I think they could have been the winner last week if they had gone ahead with a cut, but you don’t get to go back and redo. I firmly believe they will assess the situation and take the steps necessary. It takes time for their tools to work so they do need to get going. But it’s not like all is lost. They’re going to have to probably play some catch up and they won’t get to do the victory lap.

Simone Del Rosario: The Fed is finding itself back in a position that it was when it started the hiking campaign, which was that it started hiking too late and then they were doing massive hikes. There’s all this talk now about how much more they may have to cut in September and beyond. Do you think that’s overblown?

Claudia Sahm: This cycle was always going to be messy. This has been a very hard-to-read economy. If you think about it, 2022, the Fed went really fast. They raised interest rates really quickly. There were a lot of concerns that we were going to be in a recession, that that was going to be part of what we had to have happen to get inflation down because it had gone up. Well, in fact, two years later, there has been no recession and we had a big disinflation.

It was not pretty in terms of how you would necessarily want the policy to roll out, but things worked out relatively well. So just because it doesn’t have this elegant, gradual cuts, it’s about getting the job done.

It clearly creates strain on families and businesses when they see the stock market, big numbers moving and what comes next. Fear can take on a life of its own and that is something that lives around the edges and in the middle of a recession. So you don’t want to treat those dynamics lightly, but we’ve dealt with a very uncertain, hard-to-read world for the last four and a half years. So we’re not done with the drama.

It was a missed opportunity by the Fed. At least that’s what it looks like today. We’ll get inflation data next week, maybe it doesn’t. But it looks like that was a missed opportunity, but there are so many more opportunities ahead of them to do good policy.

Overreaction or rational? Here’s why the US stock market plunged Monday.

Investors slammed the sell button the morning of Monday, Aug. 5, with the Dow Jones Industrial Average sliding more than 1,000 points before the opening bell. The tech-heavy Nasdaq lost 6% while the S&P 500 was down more than 4% before the stock market opened.

The global sell-off started overseas in Japan with the Nikkei index having its worst day since 1987’s Black Monday crash. On Monday, the Nikkei plunged 12.4%.

It was Tokyo traders’ first chance to react to Friday’s U.S. jobs report, where unemployment unexpectedly spiked to 4.3%, triggering a U.S. recession indicator.

Japan’s rout was contagious and U.S. markets slid further Monday than their own initial reaction Friday, when the S&P fell 1.8%. On Monday, the market’s “fear index” surged to levels not seen since spring of 2020.

There is no doubt the sell-off is sparked by recession concerns from the jobs report and worries the Federal Reserve is way behind the eight ball when it comes to cutting rates.

“The Federal Reserve is at real risk of missing the boat, of being too late to the game when it comes to making sure that jobs continue to grow and that workers have good opportunities in the labor market,” former Acting and Deputy Labor Secretary Seth Harris told Straight Arrow News on Friday.

“We’re beginning to hear from folks on Wall Street, the R word, the discussion of recession,” Harris said. “Now, I don’t think that this report tells us that we’re headed for recession. But as folks on Wall Street begin to start talking about it, that can become a downward spiral as it becomes a decision-making point for businesses.”

“If you think that we’re going to shrink – if the economy is going to slow and shrink – you don’t invest in hiring people, you don’t invest in capital equipment, you don’t invest in expansion, you don’t invest in inventories,” Harris continued. “And so that is the concern.”

In the case Harris describes, negative conditions can become a self-fulfilling prophecy. Will cooler heads prevail? Many assessments of Monday’s sell-offs are that it is an overreaction to the data. But it is not just the labor market and Fed actions feeding into it.

For some time, investors worried tech stocks are overinflated this year, and over the weekend, Warren Buffett’s Berkshire Hathaway announced it sold nearly half its Apple stock in the second quarter. Apple started the day down 8% and dragged down Nvidia and other tech stocks with it.

Bitcoin also fell from around $62,000 Friday night to briefly under $50,000 Monday morning.

“Bitcoin doesn’t look like The New Gold,” Bloomberg Reporter Joe Weisenthal wrote. “It looks like 3 tech stocks in a trenchcoat.”

Employers added only 114,000 jobs in July, according to data released Friday, Aug. 2, by the Bureau of Labor Statistics. That number missed economists’ expectations of 175,000. Meanwhile, the unemployment rate in July ticked up to 4.3% from 4.1% in June. July marked the fourth straight month the unemployment rate rose and it is at its highest level since October 2021.

“I don’t think that this report tells us that we’re headed for recession,” former Acting and Deputy Labor Secretary Seth Harris told Straight Arrow News Friday. “The GDP [gross domestic product] numbers don’t give us any indication that we’re headed for recession. The second quarter GDP numbers were good, solid numbers; not booming, but very good for this deep into a growth cycle in the United States.”

Real GDP is estimated to have risen by 2.8% year over year, according to the “advance” estimate released by the Bureau of Economic Analysis. The official number will be released on Aug. 29.

The Sahm Rule

These latest recession fears come from what is known as the Sahm rule, developed by economist Claudia Sahm. The rule states a recession in the U.S. has started when the three-month average of the unemployment rate crosses 0.5% or more from the previous year’s low.

“I agree with Claudia about Claudia’s rule, and that is that it can be a little bit too pessimistic, particularly when you are at, historically, very, very low unemployment rates,” Harris said, referencing Sahm’s own contention that the rule could be overstated in this instance due to labor market behavior from the COVID-19 pandemic and an increase in immigration.

“We’ve seen that we had a period of more than two years of unemployment rates below 4%,” Harris told SAN. “That’s the longest period we’ve had that low [of] unemployment since the 1960s. But it shows us that our economy can be immensely successful with an unemployment rate that gets to and remains below 4%. That is where full employment begins.”

Meanwhile, Harris said movement in the markets due to an imminent recession is an “overreaction.”

“We’ve seen a meaningful sell off in equity markets around the world, not just in the United States, but certainly here in the United States over the course of the last several days, and a part of that is recession concerns, which is, in my view, a gross overreaction to what we’re seeing right now,” he said. “We certainly are not seeing numbers that suggest that a recession is imminent, or the recession is even an intermediate-term concern. It can be a longer-term concern, but I don’t think we can see it as an intermediate-term concern.”

However, Sahm herself, who stands by her statement that the U.S. is not currently in a recession despite triggering her rule, told Yahoo! Finance Friday that she is “very concerned” about a recession in the next three to six months.

Economist predicts stocks to fall 30%. Are recession fears back?

In a forecast that has reignited some economic concerns, Peter Berezin, the chief global strategist at BCA Research, anticipates a 30% decline in the S&P 500. Berezin warned of a looming recession possibly as soon as late 2024 or early 2025.

Berezin attributes his prediction to a projected slowdown in the labor market that he believes will escalate rapidly, placing immense pressure on consumer spending — an essential driver of economic activity.

Recent economic indicators have shown a mixed picture.

While Berezin’s forecast paints a gloomy outlook, not all economists share his pessimism. Some, including the chief economist at Goldman Sachs, have expressed confidence earlier that the U.S. is far from entering a recession.

Reflecting on the history of economic predictions, MIT professor Paul Samuelson’s famous quip resonates: “The stock market has predicted nine out of the last five recessions.” It underscores the challenge of accurately forecasting economic downturns.

Despite data indicating the absence of a recession currently, a recent Harris poll found that a majority of Americans believe the country is already in a recession. If Berezin’s predictions materialize, the implications could be profound, influencing upcoming elections as voters decide on leadership amid economic uncertainty.

How will banks hold up against stress test that mimics 2008 financial crisis?

Doctors use stress tests to find out how well one’s heart works when pumping harder than normal. The Federal Reserve does the same for banks and this year’s health results will be released Wednesday, June 26, after markets close.

After the 2008 financial crisis, the Fed determined it was a good idea to test how banks would hold up in the face of a severe global recession. Now, the Fed runs these stress tests annually on the nation’s biggest banks.

In this year’s fictional scenario, the unemployment rate peaks at 10%, which is what it peaked at during the Great Recession. Housing prices fall 36% and commercial real estate prices tank 40%. The largest banks are also subject to hypothetical global market shocks. In all, the Fed stress-tested 32 banks this year.

Straight Arrow News interviewed former Fed adviser and founder and CEO of QI Research, Danielle DiMartino Booth, ahead of the stress test results.

The following has been edited for length and clarity. You can watch the interview in the video at the top of this page.

Simone Del Rosario: Why should the average American care about how banks perform on these tests?

Danielle DiMartino Booth: I think what’s critical is to not have too short of a memory. I realized that 2008, 2009, at this point we’re talking almost 20 years ago. But it was very disruptive to the U.S. economy when the banks in the country were lining up like dominoes, one after the other, and effectively failing and requiring bailouts of some semblance. It was extremely disruptive to the economy.

Credit to households and businesses was abruptly cut off. That is going to be a huge impairment whether you’re running a business or if you’re trying to buy a car. We’ve seen that a hacking exercise that really run amok with the nation’s automobile dealerships was enough to kind of bring auto to its knees.

A similar set of circumstances can certainly unfold if banks end up being weaker than what we think they are and lending comes to a halt.

Simone Del Rosario: How do you think banks are going to fare when we get the results on Wednesday?

Danielle DiMartino Booth: We really are talking about the nation’s 32 largest banks. And if you could carve out the largest four banks, they have been very aggressive in recognizing losses and actually going so far as to push through charge-offs for some of their more problematic commercial real estate loans. I think that that is going to leave the very biggest U.S. banks in a good position to pass these stress tests.

When it comes to some of the mid-sized banks, I would say that’s where things might get a little bit more treacherous because some of your smaller banks that are still, nonetheless, multi-billion-dollars-in-assets banks, some of them haven’t really had the wherewithal, the ability to be that aggressive with their write-offs. So we’re kind of in a wait-and-see mode there. And we’ll see what those stress tests look like for them.

Overall though, one of my greater concerns is credit cards. I think banks have been a little bit more aggressive, surprising me, as the U.S. consumer has weakened. So I’ll be interested to see how their credit card loan books fare in the aftermath of these stress tests.

Simone Del Rosario: What are you concerned about when it comes to credit cards?

Danielle DiMartino Booth: Banks continue to grow their credit card loan books long after they had really clamped down and stopped growing their automobile loan books. And if you think about it, they walk hand in hand. If somebody is going to have trouble paying on their car loan, in many cases, they’re also going to have trouble making good on their other obligations that are in the form of debt.

And yet banks continue to increase the size of their loan books as if this fairly new phenomena of “buy now, pay later” was not running in the background and racking up about a third of whatever we were seeing increases in credit card debt on a per month basis. Buy now pay later was increasing by about a third of that growth rate, yet it’s not reflected on bank balance sheets. It’s not reported to credit agencies.

And that was really what surprised me with banks becoming as aggressive as they have their first quarter bank call sheets. It looks like they finally may have taken a step back, a little bit more risk averse on that front. I’ll be anxious to see what the Fed has to say about their credit cards.

Simone Del Rosario: Banks have gotten a lot better at passing these stress tests. Do you think there’s a chance they are too backward-looking? Let’s hope we don’t repeat the mistakes that led to the 2008 financial crisis, but are we accounting enough for future risks that are more indicative of the time that we’re living in?

Danielle DiMartino Booth: Things indeed are different. I just mentioned buy now, pay later, which certainly was not around 10, 15 years ago. And you’re right, driving through the rearview mirror can be very problematic, fighting the last war.

It remains to be seen where the true stress lies in the system. The fault lines have decidedly moved. We are a much more global and interconnected banking system than we were.

Prior to the pandemic, we heard a lot every day about de-globalization. But in the aftermath of the great financial crisis, there were a lot more entities, countries, banks and firms internationally that took out debt that was dominated in dollars. And that’s just one example that I can think up of where we might not know where the stresses lie.

We just had a very large Japanese bank declare that it was going to be sustaining very large losses based on its holdings of U.S. Treasuries.

Simone Del Rosario: Separate from these stress tests, large banks also undergo living will exercises, which test how quickly the largest banks could unwind Wall Street contracts in the event of a catastrophe. Four of the eight largest banks fell short this time around. What does that tell us?

Danielle DiMartino Booth: That tells you that bankers are really being bankers. It is a bank’s business model to have as much of their capital deployed, working for the bank, making loans, growing the asset base. That is what banks do.

It does not necessarily surprise me to hear that they have failed in writing their own wills. They have shareholders that they have to look out for, and you would normally want to see something of the nature of a will be more of a back and forth, something that is apt to be negotiated after the fact until regulators are comfortable that banks are where they need to be.

But does it surprise me that banks have not been aggressive enough? Absolutely not.

Nearly two-thirds of middle class say they are struggling financially: Poll

As the 2024 presidential election approaches, the economy is one of top issues for American voters. According to a recent poll from the National True Cost of Living Coalition, middle-class citizens report to not be doing well and they don’t expect that to change for the remainder of their lives.

According to the poll, middle class includes people making $60,000 for a family of four — 200% of the federal income poverty level. About two-thirds of middle-class Americans said they are facing “economic hardship.”

However, even for high-income Americans — people making over $150,000 for a family of four — a quarter of those polled said they also worry about paying their bills.

Overall, regardless of income level, 60% of respondents said they are financially struggling. That number coincides with the 62% of Americans saying inflation is a big problem, according to a recent Pew Research poll.

The poll from National True Cost of Living Coalition gathered more data about Americans’ financial and economic state.

40% of respondents live paycheck to paycheck.

46% do not have $500 in their bank accounts.

42% of those who want child care are stressed about affording it, with 56% unable to afford what they want.

A recent Gallup poll showed that 46% of Americans view the economy as “poor.” In a recent Harris poll, about 56% of respondents believed the country is in a recession.

However, some economic reports show positive growth in the U.S. economy. The economy and Americans’ contrasting feelings towards it are also captured when comparing campaign ads from President Joe Biden and former President Donald Trump.

“Over 12 million jobs have been created,” one campaign ad supporting Biden said. “And Joe Biden’s building an economy that leaves no city and no American behind.”

“Not one thing is cheaper under crooked Joe,” an ad from Trump declared. “Food, gasoline, cars, trucks, rent. They’re all through the roof.”

How well the economy is doing is often a numbers game. Depending on how someone interprets the data, people can reach different conclusions and have contrasting perceptions of the economy.