Jamie Dimon warns tariffs need quick resolution as banks up recession risk

JPMorgan Chase CEO Jamie Dimon cautioned that President Donald Trump’s tariff policies increase inflation and the likelihood of a recession. Chase recently put the chance of a recession this year at 60%, up from 40%.

Globally, stocks have shed trillions in value due to the threat of a large-scale trade war, with significant declines in the U.S. and Asia.

In January, Dimon downplayed the inflationary impacts of the tariffs, viewing them as a necessary cost for national security. However, his annual letter released on April 7 warned of long-term economic fragmentation from allies.

Full Story

The CEO of America’s largest bank warned tariffs put a heavy load on an already-weakening economy.

JPMorgan Chase CEO Jamie Dimon is one of the most influential voices in finance.

In his annual letter published Monday, April 7, he warned President Donald Trump’s tariff policies will increase inflation and the likelihood of a recession.

Dimon wrote that the new tariff policies interject a lot of uncertainty: potential retaliatory actions, effect on confidence, impact on investments and capital flows and possible effects on corporate profits and the U.S. dollar.

In the short run, I see this as one large additional straw on the camel’s back.

JPMorgan Chase CEO Jamie Dimon on tariffs impacting an already-weakening economy.

“The quicker this issue is resolved, the better because some of the negative effects increase cumulatively over time and would be hard to reverse. In the short run, I see this as one large additional straw on the camel’s back,” Dimon wrote.

Will it be the straw that breaks the camel’s back?

Dimon’s own bank projected a 60% chance of a global recession by the end of the year, up from the 40% previously forecast.

The threat of a large-scale trade war has hammered stocks around the world.

In the U.S., equities are having some of the worst trading days since 2020. The S&P 500, a weighted index of the 500 largest companies listed in the U.S., traded in bear market territory on Monday, April 7, after falling more than 20% from the record high hit in February.

Overseas, stocks in Asia got battered on Monday. Hong Kong’s Hang Seng Index had its worst trading day since the 1997 Asian financial crisis, falling 13.2%.

I don’t want anything to go down. But sometimes you have to take medicine to fix something.

President Donald Trump on the stock market’s response to his tariff policies

“I don’t want anything to go down. But sometimes you have to take medicine to fix something,” Trump said about the stock market aboard Air Force One on Sunday, April 6.

Trump previously refused to rule out the chance his tariff policies would cause a recession, saying the U.S. faces a “period of transition.”

Changing tune on tariffs

Dimon disapproved of Trump’s preference for tariffs in the president’s initial term. He said they threatened the economy.

However, as Trump took office for a second term in January, Dimon had a fresh take while talking with CNBC at the World Economic Forum in Davos, Switzerland.

“People are arguing, is it inflationary, is it not inflationary? I would put it in perspective. If it’s a little inflationary, but it’s good for national security, so be it. I mean, get over it,” Dimon said.

He said the outcomes depend on how the administration implements the tariffs.

“They are an economic tool, that’s it. They’re an economic weapon, depending on how you use it and why you use it and stuff like that,” Dimon said.

What changed between January and today?

In his letter, Dimon endorsed legitimate reasons to overhaul trade policy. But as the severity and targets of Trump’s tariff policies became clear, Dimon issued a few warnings.

“Economic fragmentation from our allies may be disastrous in the long run,” he wrote. “Keeping our alliances together, both militarily and economically, is essential. The opposite is precisely what our adversaries want.”

In the short term, Dimon said the country is “likely to see inflationary outcomes, not only on imported goods but on domestic prices, as input costs rise and demand increases on domestic products.”

Countries already coming to the table

The White House announced more than 50 countries have contacted the administration to negotiate trade since Trump announced the levies.

Meanwhile, the EU said it was ready to negotiate a tariff pact with the U.S. that would reduce or eliminate penalties from either side, but it also stands ready to defend its trade interests.

The S&P 500 touched bear market territory to open the trading day on Monday, April 7. Stock markets continued to trek in the red in response to President Trump’s tariffs.

Hong Kong’s Hang Seng Index had its worst trading day since 1997, dropping 13.2%.

Trump described his tariff policies as “medicine,” and the White House said more than 50 countries have reached out to negotiate trade terms.

Full Story

Stocks entered bear market territory on Monday, April 7, as investors continued dumping stock in the wake of President Donald Trump’s tariff policies. The S&P 500, Dow Jones Industrial Average and Nasdaq each fell more than 4% to start the trading day, while the S&P 500 officially traded in bear market territory.

A bear market is typically when a stock index falls 20% from a recent high. In the case of the S&P 500, a weighted index of the 500 largest companies listed in the U.S., the most recent high is the closing record of 6,144.15, hit on Feb. 19.

Minutes after the stock market opened on Monday, the S&P 500 traded below 4,915, marking a more than 20% decline. If the S&P 500 closes the trading day below that mark, it will signify a bear market.

The cause of this trek into bear market territory is straightforward. President Trump’s widespread tariff policies rocked markets after he announced them on Wednesday, April 2, and stock markets around the world have been taking a beating ever since. By Monday morning, the S&P 500 had fallen more than 12% since Wednesday’s close.

“I don’t want anything to go down. But sometimes you have to take medicine to fix something,” Trump said about the stock market aboard Air Force One on Sunday, April 6.

Some global stocks have worst day in decades

The financial fallout is not limited to the U.S. In Asia, Hong Kong’s Hang Seng Index fell 13.2% on Monday, the most significant single-day decline since the 1997 Asian financial crisis. The index includes many companies involved in global trade on the Chinese mainland.

China announced it would retaliate against Trump’s 34% tariffs by implementing 34% tariffs of its own. It also targeted some American companies and plans to restrict exports of rare earth minerals.

Over the weekend, the 10% tariff baseline on all U.S. imports took effect. The so-called reciprocal tariffs are set to take effect on Wednesday, April 9, which includes that 34% levy on Chinese goods.

The Trump administration said more than 50 countries have reached out to negotiate trade terms.

An error in the equation?

While the Trump administration long referred to the coming tariff rates on other countries as reciprocal, the calculations point to a different equation. Straight Arrow News took a look at that formula and how each country’s “tariff rate” was calculated. Essentially, the tariff rate is equal to the trade deficit divided by U.S. imports.

The conservative think tank American Enterprise Institute said the more complex equation the White House claimed to use has an error that inflates the tariff rate.

“Their mistake is that they base the elasticity on the response of retail prices to tariffs, as opposed to import prices as they should have done,” the editorial reads.

If the error is corrected, the 49% tariff rate on Cambodia would change to 13%, for example.

Goldman Sachs ups recession probability to 35% as ‘Liberation Day’ tariffs loom

Goldman Sachs has upped the probability of a recession to 35% in a research note. The bank pegged recession chances at 20% earlier in March.

Recession chatter has increased as the extent of President Donald Trump’s tariffs come into focus.

“Liberation Day” is what President Trump has dubbed the day he plans to institute a form of reciprocal tariffs. That day is Wednesday, April 2.

Full Story

One of America’s largest banks says the probability of a recession in the U.S. in the next 12 months has increased to 35%.

Goldman Sachs released the latest forecast just days before the Trump administration institutes “Liberation Day” policies.

“We now see a 12-month recession probability of 35%,” Goldman Sachs said in a research note dated March 30. “The upgrade from our previous 20% estimate (of a U.S. recession) reflects our lower growth baseline, the sharp recent deterioration in household and business confidence, and statements from White House officials indicating greater willingness to tolerate near-term economic weakness in pursuit of their policies.”

Goldman Sachs isn’t alone in its projections of a possible recession. UCLA’s Anderson School of Management issued a “recession watch” earlier in March. They said that if Trump’s proposals are fully or nearly fully enacted, it could contract enough sectors to trigger a recession in the next year or two.

What will ‘Liberation Day’ bring?

Recession talk has picked up amid the White House’s tariff campaign. The administration dubbed Wednesday, April 2, as “Liberation Day.”

“We have ‘Liberation Day,’ as you know, on April 2,” Trump said on Friday, March 28. “Many countries have taken advantage of us, the likes of which nobody even thought was possible for many, many decades, for decades. And, you know, that has to stop.”

The Trump administration has stood by the importance of its policies, even if they cause some economic pain in the near term.

“There is a period of transition because what we’re doing is very big,” President Donald Trump told Fox News on March 9. “We’re bringing wealth back to America. That’s a big thing. And there are always periods of, it takes a little time. It takes a little time.”

“These policies are the most important thing America has ever had, so it is worth it,” Commerce Secretary Howard Lutnick told CBS News in response to a question earlier in March about whether the administration’s economic policy could lead to a recession. “It is worth it. I think the only reason there could possibly be a recession is because of the Biden nonsense that we had to live with.”

Federal Reserve chair says recession risks ‘not high’

President Trump plans to roll out his latest round of tariffs on April 2. Goldman is expecting reciprocal tariffs averaging 15% across U.S. trading partners. The uncertainty around what tariff policy may be enacted caused markets to fall on Monday, March 31. The S&P 500 fell to its lowest level in six months.

“If you look at outside forecasts, forecasters have generally raised, a number of them have raised their possibility of a recession somewhat, but still at relatively moderate levels, still in the region of the traditional because they were extremely low,” Federal Reserve Chair Jerome Powell said after UCLA’s “recession watch” was issued. “If you go back two months, people were saying that the likelihood of a recession was extremely low. So it has moved up, but it’s not high.”

Core personal consumption expenditures, the Fed’s preferred inflation measure, was up 2.8% in February from the previous year. Goldman increased its PCE forecast for 2025 to 3.5%. At the same time, the bank downgraded its economic growth estimates to 1%.

“While sentiment has been a poor predictor of activity over the last few years, we are less dismissive of the recent decline because economic fundamentals are not as strong as in prior years,” Goldman added in its note.

The Conference Board’s Consumer Confidence index fell for the fourth straight month in March. Meanwhile, the expectations index, which looks at “consumers’ short-term outlook for income, business, and labor market conditions,” dropped to its lowest level in 12 years.

The latest estimate from the Atlanta Fed’s GDP forecaster has the U.S. contracting 2.8% in the first quarter of 2025. A recession is generally called when there are two consecutive quarters of negative economic growth. However, the final official decision comes from the National Bureau of Economic Research.

UAW president Shawn Fein supports Trump’s auto tariffs

Shawn Fain, president of the United Auto Workers union, applauded President Donald Trump’s move to levy 25% tariffs on all imported automobiles. However, Fain said it can’t stop there.

Fain aims to ensure American auto workers receive fair pay as more jobs return to the U.S.

Trump’s tariffs will take effect on Wednesday, April 2.

Full Story

With President Donald Trump’s new 25% tariffs on all imported automobiles set to take effect on Wednesday, April 2, the United Auto Workers union president praised the move.

What did the UAW president say?

UAW President Shawn Fain appeared on CBS’ “Face the Nation” on Sunday morning, March 30. Fain said the tariffs are a “tool” he hopes will help bring auto manufacturing back to the U.S. However, he also emphasized that the efforts cannot stop there.

“If they’re going to bring jobs back here, you know, they need to be life-sustaining jobs where people can make a good wage, a living wage, have adequate health care and have a retirement security and not have to work seven days a week or multiple jobs, just to scrape to get by, paycheck to paycheck,” Fain said.

How does that align with the Trump administration’s views?

Fain’s remarks aligned with Trump’s views, as well as those of his economic advisers.

While they acknowledged that the tariffs may cause some economic disruption in the short term, they believe they will ultimately benefit the country significantly in the long run.

Still, many economists fear the tariffs will raise costs and spur a recession in the U.S.

What about concerns over rising prices?

NBC News anchor Kristen Welker said that on Sunday’s “Meet the Press,” she spoke with Trump on the phone about the possibility of tariffs causing auto prices to rise. She reported that the president said he “couldn’t care less” if foreign automakers raised prices, saying it would lead more people to start buying American cars.

Automakers’ stocks have tumbled since Trump’s tariff announcement, affecting even U.S. manufacturers, as supply chains span across North America.

Commerce secretary: Tariff policies ‘worth it’ even if recession comes

U.S. Commerce Secretary Howard Lutnick said tariff policies are “worth it” even if they lead to a recession, two days after saying there would be no recession in America.

American banks say there is an increased risk of recession over the next 12 months.

President Donald Trump previously refused to rule out a recession as his tariff policies take effect, calling it a “period of transition” for the economy.

Full Story

U.S. Commerce Secretary Howard Lutnick said if the Trump administration’s policies lead to a short-term recession, it’s “worth it.” Lutnick’s latest comments come as the biggest banks in the nation say there is an increased chance of an economic downturn.

“These policies are the most important thing America has ever had, so it is worth it,” Lutnick said during an appearance on “CBS Evening News” on Tuesday, March 11, when asked whether President Donald Trump’s tariff policy causing a recession would be worth it.

“It is worth it,” Lutnick stated. “The only reason there could possibly be a recession is because of the Biden nonsense that we had to live with.”

The administration’s back-and-forth on tariffs has spooked the stock market in recent weeks. All three major indexes have given up gains since Trump was elected in November 2024. Still, the commerce secretary said that markets would adjust to the pace of Trump’s policy.

“Markets are going to learn,” Lutnick said Tuesday. “Let the dealmaker make his deals. Let the best negotiator and the best person who cares about America, let him make the deals.”

Economists say recession chances are rising

As markets fall and economic policy is uncertain, recession talk has picked up. Goldman Sachs recently increased the odds of a recession from 15% to 20%. Meanwhile, economists at JPMorgan say there’s a 40% chance of recession in 2025.

“I do think the likelihood of a recession has risen,” Morgan Stanley’s Chief U.S. Economist Michael Gapen told NPR Tuesday. “Pegging it to a particular probability is hard. Maybe 20%-25%, so maybe twice as high as you might have in any normal given year. So the probability has risen, given the combination of policies, tariffs, spending cuts, immigration controls, which all tend to soften activity in the near term.”

Tariffs impact the cost of goods

Gapen told NPR that tariffs are essentially a tax on American citizens.

“Tariffs are essentially a tax on consumption — you pay more to import that good, so the cost to the consumer ends up rising,” he said.

“So one of the simple tenets of economics is if you make something more expensive, you get less of it,” Gapen added. “So less trade activity tends to mean growth is a little softer. But you impose tariffs, it tends to push inflation higher in the short run. So that’s the balance we’re considering.”

Tariffs cause a ‘period of transition,’ so what’s the end game?

“You would hope the costs you pay in the short run are outweighed by the gains in the long run, but those short-run costs tend to be more obvious,” Gapen said. “The gains over time, we’re never quite sure if they materialize. But that is, I think, the argument they’re making and why we might see some softness in the near term.”

In the latest running estimate by the Federal Reserve Bank of Atlanta’s GDP tracker, the economy is headed for a 2.4% contraction in the first quarter of 2025. That’s a significant swing from the end of January when it was pacing for 2.9% growth.

A recession typically occurs when there are two consecutive quarters of economic decline. However, the final call goes to a panel at the National Bureau of Economic Research.

“Here’s what happens when you say we’re going to have a tariff on April 2,” Lutnick said Tuesday. “Everybody tries to hustle in before the tariff. So there’s lots and lots, and you could see miles of cars coming into the country to try to beat the tariff from Japan, from Korea and from Germany.”

“That creates a distorted GDP,” he continued. “It doesn’t change a darn thing about America. Americans are going to see American cars are going to be cheaper than foreign cars, and the people who make those American cars are going to be American, and these things are great for America.”

Stock market continues its dive as Trump leaves recession on the table

The Dow tumbled nearly 900 points and the Nasdaq just had its worst trading day since 2022 as stocks roiled Monday, March 10.

President Donald Trump declined to rule out an upcoming recession during an interview that aired Sunday. The comments come as the stock market was already sinking with uncertainty over the administration’s tariff policies.

U.S. Commerce Secretary Howard Lutnick firmly wrote off the chance of a recession.

“I hate to predict things like that,” he said in response to a question from Bartiromo about whether there would be a recession. “There is a period of transition because what we’re doing is very big. We’re bringing wealth back to America. That’s a big thing. It takes a little time.”

But some in the Trump administration are more definitive when it comes to questions about a recession.

“Donald Trump is a winner; he’s going to win for the American people,” Commerce Secretary Howard Lutnick said during an appearance on NBC’s “Meet the Press” on Sunday, March 9. “That’s just the way it’s going to be. There’s going to be no recession in America.”

Stock market sinks on Trump’s comments, tariff developments

All three major stock market indexes sank on Monday, March 10, as investors are rattled about what the future holds regarding tariffs.

The Nasdaq had its worst day since 2022, dropping 4% in a single day. The S&P 500 dropped 2.7%, while the Dow Jones Industrial Average fell nearly 900 points, closing about 2.1% down.

A recent survey of economists from the U.S., Canada and Mexico by Reuters found 70 of the 74 polled said the risk of recession in their economies has increased.

“I wanted to help Mexico and Canada to a certain extent. We’re a big, big country, and they do a lot of their business with us, whereas in our case, it’s much less significant,” Trump said in the Sunday interview. “And I wanted to help the American car makers until April 2.”

Election gains wiped from the board

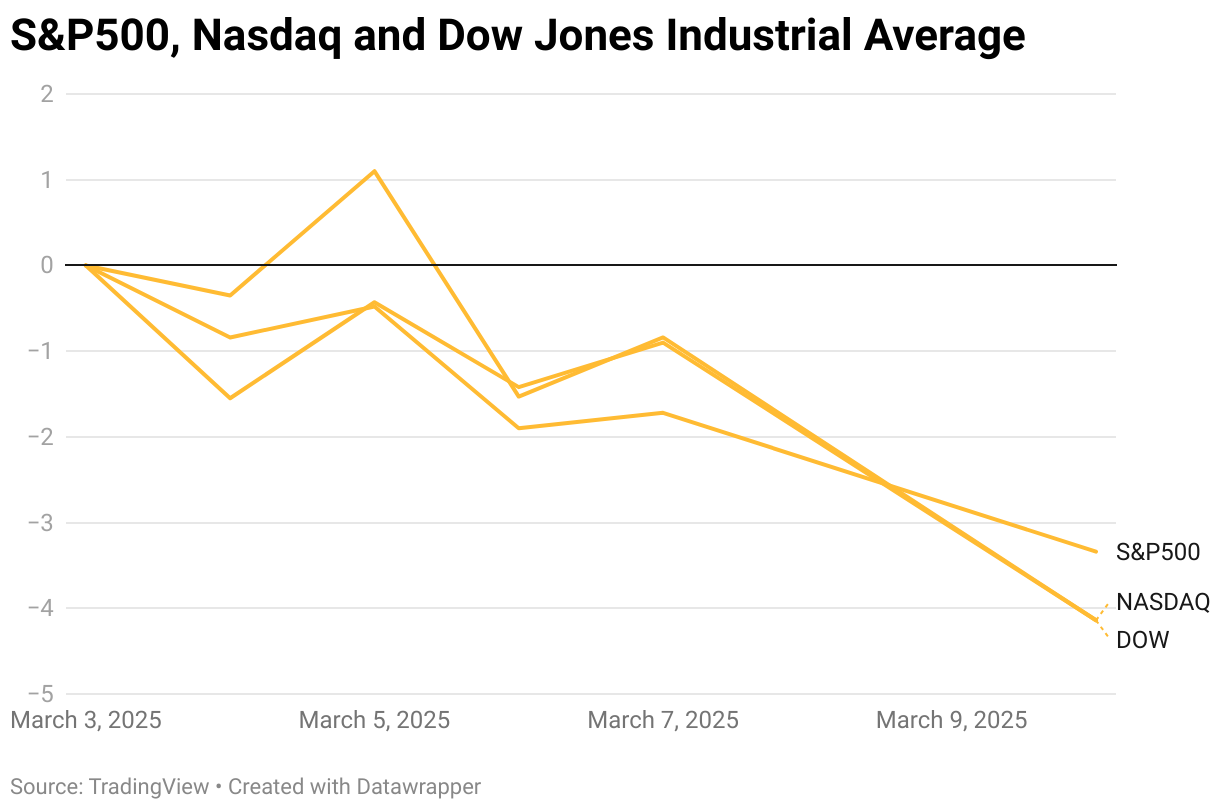

Markets have been reeling in recent weeks as investors worry about the impact the president’s tariffs could have on U.S. consumers and the economy as a whole. During the week of March 3, the S&P 500 and tech-heavy Nasdaq each lost more than 3%. Meanwhile, the Dow fell 2.4%.

Markets surged after Trump won the election in November. As of Monday, the S&P 500 and Nasdaq have given up all of those gains and are now below where they were on Election Day.

“What I have to do is build a strong country. You can’t really watch the stock market,” Trump said of recent swings in equity markets. “If you look at China, they have [a] 100-year perspective. We go by quarters.”

But two consecutive quarters of economic contraction doesn’t necessarily signify a recession these days. A group of eight economists at the National Bureau of Economic Research are tasked with taking a more nuanced approach to declaring an official recession. The experts who make the decision say a recession “involves a significant decline in economic activity that is spread across the economy and lasts more than a few months.”

‘Recession pop’: Can great music signal an economic downturn?

It’s tough to identify if the economy is in a recession. Economists toil over economic data to try to find the most accurate indicators. Gross domestic product and unemployment numbers are great data points, but what does the state of pop music tell us about economic conditions?

Traditionally, two consecutive quarters of negative growth is the preferred method to tell a recession took place. When it comes to unemployment, the Sahm Rule is triggered when the three-month moving average of the unemployment rate is half a percentage point above the 12-month low. The McKelvey Rule is essentially the same but is triggered when the unemployment rate is 0.3 percentage points above the 12-month low. The inverted yield curve, when short-term Treasury yields exceed long-term yields, is also a recession indicator.

Exploring Recession Pop: A Journey Through Music and Hardship * Recession Pop, characterized by its upbeat and escapist dance music, emerges during times of economic turmoil as a form of distraction and catharsis. * This phenomenon is not new, with historical examples dating back to the Great Depression and recurring during subsequent periods of hardship. Pre-Recession Examples: * Dance music as a form of escapism can be traced back to the Great Depression era, where swing and jazz provided solace amidst economic struggles. * In the UK, the Winter of Discontent in 1978/1979 saw the rise of ABBA’s albums, offering a similar escape during a period of social and economic unrest. The Great Recession (2000s): * The late 2000s Great Recession saw a surge in dance-pop music, offering a distraction from economic woes. * Artists like Black Eyed Peas, Rihanna, Katy Perry, and Lady Gaga dominated the charts with infectious hits. * Songs like Flo Rida’s “Club Can’t Handle Me” provided a sense of camaraderie and hope amid uncertainty, embodying the spirit of Recession Pop. * Dance music acts as a survival mechanism, providing a temporary reprieve from the harsh realities of the world. Post-Pandemic (2020s): * The COVID-19 pandemic brought about a resurgence of dance-pop and disco music, echoing the Recession Pop trend. * Artists like Dua Lipa, Doja Cat, and Beyoncé spearheaded this revival, offering upbeat and nostalgic tunes during difficult times. * Sample-heavy tracks and uplifting beats became prevalent, serving as a source of comfort and nostalgia for listeners. * Despite the challenging circumstances, the music industry continued to thrive, providing a beacon of light in dark times. * Recession Pop reflects the resilience of music as a form of escapism and catharsis during times of hardship. * Despite economic downturns and global crises, dance-pop music remains a source of joy and unity for listeners worldwide. * As we navigate through uncertain times, the enduring popularity of Recession Pop serves as a reminder of the power of music to uplift and inspire in the face of adversity. #JoesAlternativeHistory#RecessionPop#MusicHistory#GreatRecession#LadyGaga#2000sPop#BlackEyedPeas#BoomBoomPow#WinterOfDiscontent#GreatDepression#DuaLipa#Beyonce#DojaCat#ABBA#PopCulture#PopCultureHistory#recession

But then there is the notion that “pop music is brilliant” when the economy is about to face serious problems. That is where the idea of “recession pop” comes into play.

What is recession pop?

In short, recession pop is seen as the Top 40 hits that are released during an economic downturn. The most clear example was during the Great Recession.

“I would define recession pop from the years just leading up to the recession, so the end of 2007 probably at least through 2012,” Charlie Harding, an NYU Professor and co-host of the podcast “Switched on Pop,” said.

Meanwhile, Joe Bennett, a musicologist and professor at Berklee College of Music, said it’s a label that applies “to a particular body of work, which I would broadly describe as super cheerful dance floor bangers that came out sometime between 2008 and 2011.”

Super cheerful dance floor bangers that came out sometime between 2008 and 2011.

Musicologist Joe Bennett describing recession pop

Since it is not a particularly scientific indicator, Harding said the recession pop label could even go all the way into 2014 because “lots of people were still really feeling that recession well into the early 2010s.”

Is recession pop a real thing?

It’s hard to officially quantify whether pop music really reflects the economic times, but both Harding and Bennett said the interpretation is often up to the listener.

“You can find what we might say are reflective songs, where the dark times people are experiencing are indeed dealt with within the song lyric,” Bennett said. “And we might also find what you might call escapist songs. ‘What the heck, let’s party.’”

“So songwriters are not necessarily social commenters, but like all of us, everyone who creates popular culture, they are living in that culture at the time they are making the object and the market that is the pop music fans who are buying or streaming the single are also in that social context and liking what they like in the context that they’re in,” he continued.

“As much intention as a songwriter might have, whatever they might intend, the listener is going to take it and do what they want with it,” Harding added. “A great example of listeners completely misusing a song would be ‘Hey Ya’ by OutKast, which is one of the most requested songs at weddings, and yet the song is about relationships that never last.”

“The recession affected different people very differently,” Harding said. “If you lost your home, you’re gonna remember what that song is on the radio when you had to pack up and leave. It’s really different than maybe someone for whom their family got through it okay, and they’re just like, ‘I just love my recession pop bops.’”

The history of popular music is littered with songs known as “party anthems.” But the recession pop era may have had less economic-based reasons for those hits.

“I think there’s ways in which the music was great, and I think there’s other ways in which it feels a little bit reductive,” Harding told Straight Arrow News. “We’re talking about a period in which the digitization of music was fully taking over.”

Despite the idea that recession pop is specific to the Great Recession, Bennett points to music that came out amid the Great Depression to illustrate how music reflects the times.

“Bing Crosby’s ‘Brother Can You Spare a Dime?’: it was a big hit in the early ’30s, and that’s a song about a returning war veteran who’s homeless and looking for money,” he said. “In 1933, Ginger Rogers has a hit with ‘We’re in the Money.’ Is that sort of an ironic title? It’s certainly a very cheerful lyric. Maybe it’s a fantasy about having money, because a lot of people wouldn’t have in the U.S. in the early 30s.”

Nostalgia effect

With all the evidence to support the idea of recession pop, it’s hard to say one era’s music is better than another, which can make it a particularly difficult economic indicator to nail down.

“If recession pop is a nostalgic way of looking back and trying to make sense of this period of total dislocation and fragmentation, all the power to listeners to call this stuff recession pop, even if it just happened to be the upbeat, fun thing that was occurring at that time,” Harding said. “People are trying to make this connection to music that happened 10 to 15 years ago.”

There is good reason for music dubbed recession pop to be resonating with people in their 30s that may have nothing to do with the quality of the tunes or state of the economy.

“It fits with the general cycle of popular music nostalgia,” Bennett said.

Bennet added most people believe the best music was released when they were 17 years old.

“A lot of the psychology research into nostalgia suggests that it works on something like a 15-year cycle,” Bennet continued.

“It’s more of an after-the-fact analysis, which is a fun and useful way of creating playlists: being nostalgic, digging into our memory, perhaps making sense of an era that was really dark and challenging for people and making light of it after the fact,” Harding said.

Pop music today

While recession pop is likely just a label put on music after the fact, it gives us an opportunity to look at what makes a hit song and how that has changed in the last 15 years.

“I think what makes a great pop song is accessibility,” Bennett said. “Particularly if you’re releasing a single, you want it to appeal to millions of people.”

“It has to have an amazing concept,” Harding added. “[It] has to have a memorable hook, and it has to capture the zeitgeist.”

Harding likens making a great pop song to winning the lottery. Many wonder how some artists have been able to hit the jackpot over and over again. But what makes a great pop song has changed over time. Today, more and more records are being discovered on short-form video apps like TikTok and Instagram.

“TikTok is a much faster-moving medium so people need to grab their audience’s attention to stop them from vertically scrolling onto the next thing,” Bennett said of the app that broke artists like Lil’ Nas X. “As we know from TikTok, that sort of meme community will often seize on a particular part of the song, a particular audio excerpt, and use that to make its meme, its dance routine, whatever it is.”

But even though artists need to get to the hook quicker than ever before, Harding said they have more to say than ever before.

“There is this expectation that we are more giving of ourselves in our lyrics today,” Harding said. “And so I think of an artist like Charlie XCX, who, on ‘Brat,’ talked about how she wanted to write lyrics that were as if she was just texting a friend. And this is the album that has broken through for her, because some of these lyrics, they don’t have these perfect rhymes. They have the perfect imperfections.”

And there’s no bigger artist giving themselves to their music than Taylor Swift.

“I think on a lot of metrics, Taylor Swift is the biggest artist to have ever lived, in terms of the longevity of her career; the fact that she is what should be a late-stage career artist, and yet she is at her peak,” Harding said. “She has had multiple peaks that just keep getting bigger and bigger and bigger.”

Meanwhile, Bennett pointed out that Swift herself was not immune to the recession pop movement.

“Her two significant albums at that time would have been ‘Fearless,’ which came out in 2008 and then ‘Speak Now,’ which originally came out in 2010,” Bennett said. “And of course, both of those contain a whole bunch of songs in that vein: ‘Love Story,’ ‘You Belong with Me,’ ‘White Horse,’ ‘The Story of Us.’”

In the end, while there may not be a deliberate intention to make music that makes listeners feel good or sad during tough economic times, it’s clear music resonates with people and reminds them of those snapshots in time.

Fed expected to slash rates by 25 bps in September. What’s next?

After the Wednesday, Sept. 11, inflation report came in on target, markets are even more confident the Federal Reserve will cut its rate by 25 basis points following its policy meeting next week. In August, Fed Chair Jerome Powell said it was time for policy to adjust after an “unmistakable” weakening in the labor market. But how much adjusting is coming down the pike after September?

The federal fund target range is a benchmark rate for lending. Since July 2023, the Federal Open Market Committee has held the range between 5.25% and 5.5%, its highest level in more than two decades.

Markets initially expected rate cuts to come much earlier in the year, but after inflation remained stickier than anticipated, September would mark the first rate cut since early 2020 after five straight months of cooling consumer price inflation.

If the Fed decides to cut in September, it will mark the beginning of a rate-cut cycle. After the Fed’s decision on Sept. 18, the committee will meet two more times in 2024, the two days after the November election and Dec. 17-18. For more on how much the Fed may cut this year and next, Straight Arrow News spoke with the Fed Guy Joseph Wang.

The following transcript is edited for length and clarity. Watch the full clip in the video above and catch the entire interview on Straight Arrow News’ YouTube page.

Joseph Wang: So the market is pricing in a very, very aggressive Fed cut cycle, so aggressive that the market is pricing by the end of next year, the overnight rate will be below 3%. So that’s from 5.5% today to below 3% next year.

Now that’s a very aggressive rate path, expected policy pricing by the market, and that seems to assume a significant deterioration in the economy.

Let’s look at the big picture, though. The most recent GDP statistics in the US were revised upwards from 2.8% annual growth rate to 3%, so the economy is actually growing fine. There’s really no indication that we would just suddenly go from 3% to a recession where we don’t grow, we shrink.

Jobs reports, again, slowing, but we’re still creating over 100,000 jobs a month. When we’re in a recession, we don’t create 100,000 jobs a month, we lose 100,000 jobs a month. And so the pricing in the market seems to be pretty aggressive from my perspective, I think there’s too much doom and gloom being priced in.

My base case expectation is that rather than having a series of huge cuts that the market is assuming that we have, [we have] some steady 25-basis-point cuts, and maybe the cut cycle ends, let’s say around 3.5%, rather than below 3%. I say this because, by all indications, the economy continues to have momentum and there’s a good case to be made that rather than falling into recession, we really are just normalizing now.

One other thing that I would mention is that something that’s happening today that hasn’t happened before is that we have tremendous amounts of fiscal spending. The government is expected to have a fiscal deficit of about a couple trillion dollars, basically forever, and when you have the government spending so much each year, that’s very supportive of demand. It’s upward pressure on inflation. It’s not a very good management of the currency, but it is supportive of demand.

And so when you have that kind of fiscal spending, I think that’s a good tailwind. Now, one other thing to keep in mind is that what happens in November could have very big implications for macro policy. We have two candidates with very, very different visions of the world. We also have to look at Congress to see whether or not they are able to carry out their different visions of the world.

So there’s a lot of uncertainty there. But based on what I see right now, the economy is still okay, and the rate cuts in the markets are too aggressive. We’ll have some, but it doesn’t seem like we would have so many, because it doesn’t seem like at the moment that we are tumbling into recession.

Core inflation is still above 3%: Is it time for the Fed to move its target?

Inflation cooled for the fifth straight month in August at 2.5%, inching closer to the Federal Reserve’s target of 2%. But core prices, which strip out food and energy, stayed stagnant at 3.2%. Is it time for the central bank to adjust its core inflation target of 2%?

The Federal Reserve has a dual mandate of full employment and price stability. To keep those numbers in line with a strong economy, they use tools like adjusting the federal funds rate, which is the overnight lending rate for banks but in a downstream way that affects interest rates on everything from mortgages to car loans.

The range is currently set at 5.25-5.50% after the Fed raised rates from near zero starting in March 2022 through July 2023. The Federal Open Market Committee will meet next week and is expected to start cutting interest rates for the first time this year.

While it seems like the 2.5% increase in consumer prices would give Fed Chair Jerome Powell a little cover, the central bank puts the focus on core inflation, which strips out volatile food and energy prices. Core inflation is still at 3.2% annually due mainly to rising shelter costs.

Straight Arrow News interviewed Monetary Macro CIO and the Fed Guy Joseph Wang Wednesday morning, Sept. 11, to discuss the latest inflation data. The conversation turned to whether the 2% target is a realistic endgame.

The following transcript is edited for length and clarity. Watch the full clip in the video above and catch the entire interview on SAN’s YouTube page.

Joseph Wang: I think we might be in a new, higher inflation regime. So we have to be careful. The future does not always look like the past. Over the past 20 years, we’ve had a world where inflation was pretty stable around 2%, but it wasn’t always like that.

Before the “Great Moderation” period, we were in the 1970s and 80s where inflation was volatile and sometimes very high. I think we’re heading into an era where inflation is probably going to be more volatile and higher than it was in the past. That’s certainly what the CPI is telling me.

Now looking on a year-over-year basis, we’ve been above 3% for some time and honestly, it looks kind of stuck there. Now we could have recessions that temporarily bring that down, but I think the next time we have a recession, maybe we just have more stimulus checks and so forth, and that makes it surge again.

So I think the future is going to be a world where inflation is going to be higher and more volatile. And that’s something that we’re going to have to get used to.

Simone Del Rosario: Fed Chair Jerome Powell gets asked this a lot and he loves to slap this down, which is, “Is the 2% target rate out of date and should we be looking at a 3% target?”

I know Jay Powell continues to stick to his 2% conviction but are you hearing anything different?

Joseph Wang: We have to realize that the 2% inflation target is nothing magical. It’s nothing set in stone. It’s a decision made by people. Now, in the Fed’s case, it was decided in 2012 to have an inflation target of 2%. Does it have to be that way? We could easily change it.

I think it’s helpful to understand why we might want to change the target. Traditionally speaking, economists think there’s a trade off between inflation and unemployment. So they would think that if we have 3% inflation, in order to get 3% inflation down to 2%, we have to have a bit of a recession, we have to have the unemployment rate go up a little bit. So ultimately, whether or not we decide to have a higher inflation target is a political decision as to whether or not the government can tolerate a temporary recession.

When inflation was around 4% and it looked like it would have come down, there were actually many people, influential people, writing columns in big newspapers saying, “Hey, why don’t we just change the inflation target so that it’s 3% or maybe a little bit more, instead of 2%?” They were saying this because they did not want the political costs of having temporarily higher unemployment, of creating a recession. So whether or not we change the inflation target is ultimately going to depend upon the political appetite for economic weakness.

Honestly, at 3% inflation, I think that’s close enough to 2% that people would just kind of struggle and say, “Yeah, it’ll eventually get there,” and they won’t have to change the target. But the next economic cycle, when we have an upswing, maybe inflation goes back to 4%, maybe a little bit more. Depending on who’s in power, maybe they don’t want to take that risk of having a recession to get inflation down, and maybe at that time, we’ll have some serious conversations within the government about whether or not they could change the inflation target.

To your point about what the Fed people have been talking about now, definitely they would never say that they’re going to raise the inflation target. But at the moment, they are having a discussion about their framework and that’s due to be released in a couple years.

There are former Fed speakers who are whispering that, “Instead of having a 2% inflation target, what if we have something called an inflation band?” So what that means is that my target is not a 2% point, but maybe it’s 2% plus or minus 1%. So that means that inflation at 1.5% is within the band, it’s okay. If it’s 2.5% or even 3%, that’s okay as well.

So that could be a way to, by sleight of hand, increase the inflation target simply by tolerating inflation higher than 2% because it’s still within the band. That is something that people discussed before in the Fed and now they’re discussing again. I don’t know what they will ultimately decide. I think it might depend upon just how easy they think it is to maintain 2% in the coming years.

Americans surprise with confidence in economy though job concerns grow

Americans are more confident in the economy than analysts expected and that confidence has been growing throughout the summer. The Conference Board released its consumer confidence survey for August, with a 103.3 rating, beating the 100.7 expected and exceeding July’s 101.9 surprise.

It’s the highest confidence rating in months, but there’s more behind the headline number.

Conference Board Chief Economist Dana Peterson said that while consumers are more positive about business conditions now and in the future, they’re also more concerned about the labor market.

In July, unemployment rose to 4.3%. In August, fewer people told the Conference Board jobs were “plentiful” while slightly more said jobs were “hard to get.” Fewer people also expected their incomes to increase this year, while more expected their incomes to decrease.

That said, Americans’ inflation expectations dropped to their lowest level since March 2020. That comes as the Federal Reserve’s own inflation expectations are getting more rosy, as Fed Chair Jerome Powell addressed in his Jackson Hole speech last week.

“Inflation is now much closer to our objective, with prices having risen 2.5% over the past 12 months,” Powell said. “After a pause earlier this year, progress toward our 2% objective has resumed. My confidence has grown that inflation is on a sustainable path back to 2%.”

“He is confident now, not just waiting for more confidence, but confident that inflation is moving lower,” Central Bank Central Editor-in-Chief Kathleen Hays emphasized in an interview with Straight Arrow News. “It’s heading for that 2% target. And the concern is unemployment.”

Powell’s speech signaled a likely rate cut coming in September, and Americans are expecting interest rates to decline. That expectation, however, hasn’t made Americans rethink buying homes. Average responses over the past six months show plans to purchase homes are at a new 12-year low. But Americans are planning more smaller purchases. Buying plans for cars, refrigerators, TVs, washing machines, smartphones and laptops all increased.

Overall, Americans are feeling better about their family’s financial situation moving forward. They don’t see the results of the election causing much volatility in the economy and recession expectations are unchanged in August and well below 2023’s peak.

But confidence can be drawn along income lines. Those making less than $25,000 are feeling less confident overall, while those making more than $100,000 are the most optimistic.

Businesses, investors and the Federal Reserve all pay close attention to measures of consumer confidence. It’s a window into how much buying power Americans are comfortable yielding, and household spending accounts for more than two-thirds of the U.S. economy.