Will those looking to buy a car ever catch a break? With interest rates around 7% and average monthly payments above $700, it has never been more expensive to buy and finance a new car while affordable used cars remain hard to find.

A glimmer of hope has arrived for hopeful buyers: According to a recent UBS report, global automakers are overproducing, which could lead to an excess of 5 million vehicles and price cuts to clear lots later this year. But a looming strike could throw a wrench in it all.

United Auto Workers vote to strike the ‘Big Three‘

The United Auto Workers union voted Friday, Aug. 25, to authorize a strike against Detroit’s “Big Three” – General Motors, Ford Motor Co. and Stellantis, the Jeep and Chrysler maker – if contracts aren’t reached by Sept. 14.

Union president Shawn Fain said on behalf of the 150,000 workers, he is calling for 46% raises, the return of traditional pensions and 32-hour work weeks. The UAW has never had strikes for all three houses at the same time.

“There might not be any impact right away, but eventually what that would lead to is something that we saw about a year ago and maybe even back into the pandemic era,” said Brian Moody, executive editor at AutoTrader.com. “The way it will impact consumers is the prices will eventually go up and they may not be able to find exactly what they want. Again, not dissimilar to what we were seeing about a year ago.”

For now, Moody said there’s an abundant supply of vehicles and it would take some time for supply to be constrained in the event of a strike.

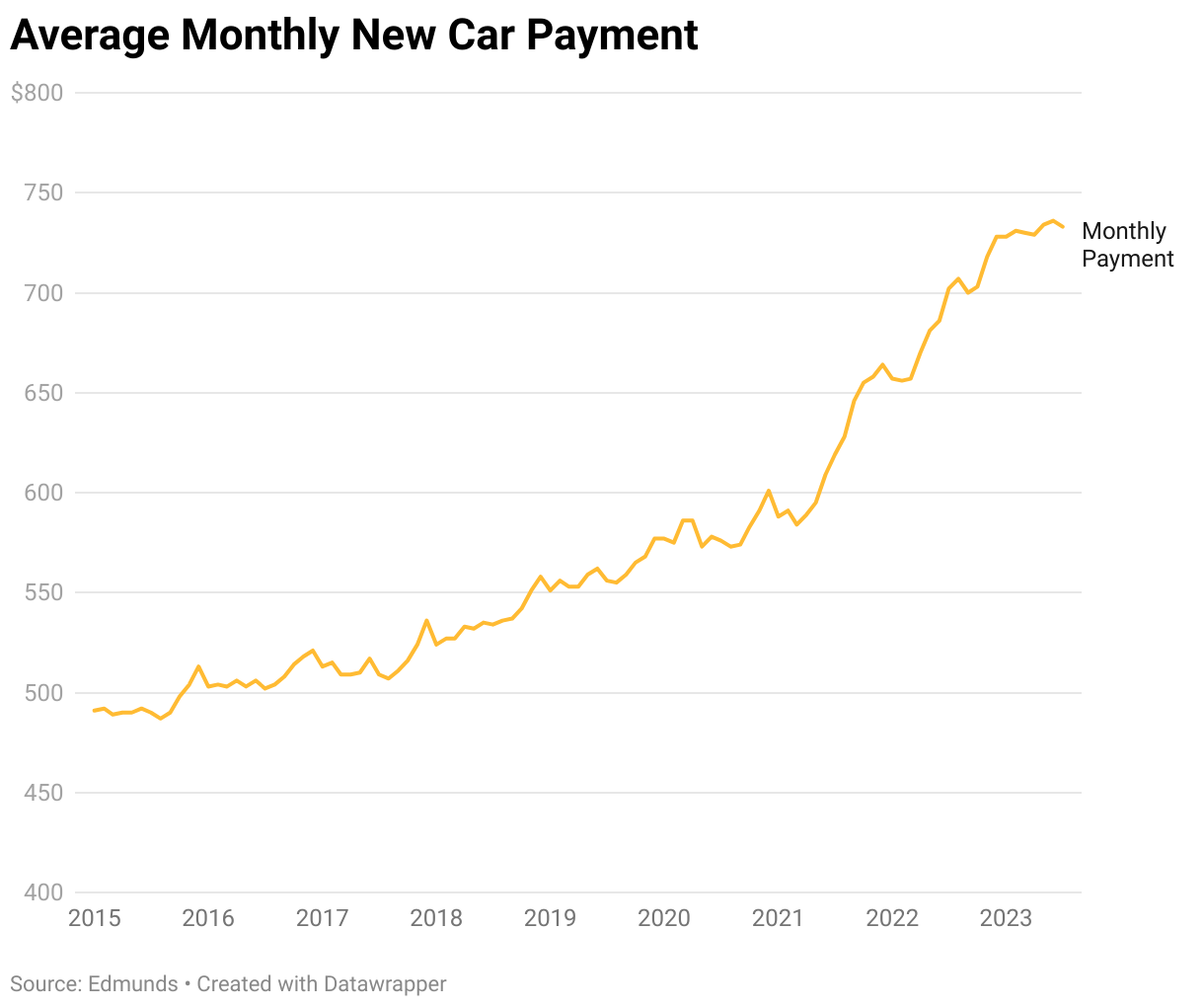

Average auto loan payments accelerating

As of July 2023, the average monthly new car payment is $733 a month, a 37% increase in the past 5 years, according to Edmunds. The figure marks roughly 15% of the average pre-tax salary, while experts suggest spending no more than 15% of take-home pay.

A lot of the increase is certainly tied to rising car prices and rising interest rates. But Moody said buyers are also overextending themselves.

“A lot of people who are buying a new car are opting for a luxury brand,” he said, pointing to a rise in luxury market share. He said based on the data, buyers are also leveling up in trim, even in lower-priced models.

Edmunds reported that more than 1 in 6 people – 17.1% – who financed a vehicle in the second quarter of 2023 have a monthly payment of $1,000 or more, an all-time peak. In the second quarter of 2019, only 4.3% of people financed a vehicle with a monthly payment reaching or exceeding $1,000.

“That’s crazy,” Moody said. “The idea that people are maybe overextending themselves with $1,000-a-month car payments, I think that’s concerning.”

Hunting for used cars

The average used car payment is $569, compared with a new car payment of $733, Edmunds reports. But finding a used car, especially a near-new car, is proving more difficult these days.

One factor is similar to what’s being experienced in the housing market: Prior interest rates are so much more favorable that auto owners aren’t interested in trading up and facing higher rates.

“But there’s also the fact that the cars are more reliable. The average used car on the road right now is about 12 years old. That means that those cars are working for them right now,” Moody said.

He also added that price point is key to selection.

“The more expensive the used car, the more abundant the supply, the more inexpensive the used car, the harder those are to come by,” he said. “There are very few cars available across the country if you’re looking for something under $10,000. If you’re looking for something over $30,000, you’re gonna have plenty to pick from.”

Auto loan delinquencies are at 7.3%, above pre-pandemic levels. Is it alarming? Brian Moody gives his thoughts in the video above.

Tags: Auto industry, Car loans, Ford, General Motors, Interest rates, Stellantis, Strike, UBS, United Auto Workers

Simone Del Rosario: Will those looking to buy a car ever catch a break? With interest rates around 7% and monthly payments above $700, it has never been more expensive to buy and finance a new car. And affordable used cars are hard to find. A glimmer of hope is here. UBS believes global automakers are overproducing, which could lead to an excess of 5 million vehicles and price cuts to clear those lots. But a looming strike could throw a wrench in at all. Brian Moody, executive editor at autotrader.com, is here to help us sort it out. Brian, we wanted you on to talk all things trends happening in the auto industry right now. But before we get into all of that I need to bring up this threatened strike happening with United Auto Workers, the chief of the Union, they’re demanding a 46% raise for their 150,000 workers return to traditional pensions and a 32 hour work week, they’re talking about possibly striking three groups at the same time, GM, Ford and Stellantis. How would this disrupt the auto industry, from a consumer perspective, if this were to go through on September 14?

Brian Moody: Well, one thing is that might not be any impact right away. But eventually, what that would lead to is something that we saw about a year ago, and maybe even back into the sort of more pandemic era, whenever you start to lose supply, or you’re low on product. That’s a problem for consumers, because what will happen is, the prices will go up, that’s usually what happens there won’t be as abundant of a supply of new cars, especially but then later, they’ll have a sort of a delayed effect with a less abundant supply of used cars, which is what we’re seeing right now. So the way it will impact consumers is the prices will eventually go up. And they may not be able to find exactly what they want, again, not dissimilar to what we were seeing about a year ago.

Simone Del Rosario: Say the strike doesn’t happen. Can people expect car prices to go down? And how much of a difference would that make given how high interest rates are right now?

Brian Moody: It will make somewhat of a difference. So what’s difficult to understand about the new car prices is they’re trending down. But the most recent data we have says that they went up slightly. When I say slightly, I mean less than 1%. That’s the smallest increase in more than a decade. So that’s not a significant enough number to worry about. So they are trending downward. Same with used car prices used car prices are kind of down. But that’s again, a delayed reaction from the low wholesale prices. We saw the beginning of summer. Now we’re seeing higher wholesale prices for used cars. So we expect that the prices of used cars will toward the end of the year, probably ramp up a little bit.

Simone Del Rosario: What are these high interest rates doing to the market? You look at the average monthly payment right now Americans are looking at $733 a month for their payment for a new car. That’s according to Edmunds, which is just so high, I think the experts would advise not to spend more than 15% of your take home pay on a used car that is 15% of the average pay before taxes are taken out. It’s obviously not advised to be spending that kind of money, but that’s what people are looking at.

Brian Moody: Yeah, you know, part of it is that the prices are simply higher from say 2020 2021 There’s no doubt about that. You can look at the graph and see that the prices went up. But also, some buyers are overextending themselves, we see certain things little indicators like that the luxury market in terms of new cars is near 20%. That’s very high. That means a lot of people who are buying a new car are opting for a luxury brand. Another thing that’s kind of telling is that we just saw that there was only one model transacting under $20,000. And that was a Mitsubishi. It doesn’t mean that there aren’t cars for sale under $20,000. There are plenty at or below the $20,000 mark, the Nissan Versa the Hyundai venue. The Kia, there’s plenty of examples of those. But what it says is so you have these cars that are priced around 20,000 doors but transacting above means people are opting for more options, or the dealers simply aren’t stocking the low price models. Both of those things could be true, but we do see that consumers are asking for higher and higher trim levels. Look at Toyota for example, they recently added an even nicer trim level on top of the already premium platinum now they have Capstone Oh, why are they doing that? Because people are asking for it.

Simone Del Rosario: And they’re willing to spend the money, I guess, uh, the amount of people that are spending more than $1,000 a month on their monthly payment at 18%. Now, I mean, it’s a crazy amount of money to be spending every single month on a vehicle. Talk to me about the the market of near New cars is that is what we’re seeing happen in the housing industry right now where people are holding on to those low mortgage rates and not wanting to sell their homes. Are we seeing the same thing happen with cars where people have a more favorable loan rate? And yes, hang onto those vehicles instead of maybe turning them around as quickly as we used to?

Brian Moody: Yes but there’s also the fact like what you said is exactly right, the interest rates are low, so holding on to him. But there’s also the fact that the cars are more reliable. The average used car on the road right now is about 12 years old. And that means that those cars are working for them right now. One of the interesting things we see with when it comes to used cars is that I gotta make sure I say this correctly is that is the more expensive the used car, the more abundant the supply, the more inexpensive of a used car, the harder those are to come by. So there’s very few cars available across the country, if you’re looking for something under $10,000, if you’re looking for something over $30,000, you’re gonna have plenty to pick from. So that’s the irony of that as the people are holding on to their cars. And yet, it’s the expensive used cars that are abundant. The whole point of getting used cars with you want to save money. So there is ways there are ways to do that. Incentives help with that. Also not getting all the bells and whistles helps with that. Also not getting full size SUVs and trucks. People always say things like, I’m looking for a great deal. And then you give them some pointers. Oh, you should do this. There’s that. Yeah, I’m thinking about getting a Yukon Denali. You’re not looking for a deal. You’re looking for the nicest car you can afford. That’s different than getting a great deal.

Simone Del Rosario: Yeah, and you talked about people overextending themselves a little bit, we’re seeing new auto loan delinquencies hit 7.3%. That is above pre pandemic levels. Are you concerned about any trends that we’re seeing here?

Brian Moody: They’re up a little bit, but I don’t think they’re up to the point of it being alarming. So this is typically a low number, but it is trending up like you said, so it’s something to keep an eye on. But I don’t think it’s an emergency right now. However, the numbers that you just gave, and the idea that people are maybe overextending themselves with $1,000 a month car payments. I think that’s concerning.

Simone Del Rosario: Brian Moody from autotrader.com Thank you so much for your expertise today.

Brian Moody: Great. Thank you.

Straight to your inbox.

By entering your email, you agree to the Terms & Conditions and acknowledge the Privacy Policy.